Capital Gains Tax is a tax on the profit when you sell an asset that’s increased in value. It is the financial gain or profit you make that is taxed, not the amount of money you receive altogether.

Some assets are tax-free. If all your gains in a year are under your tax-free allowance, you do not have to pay Capital Gains Tax.

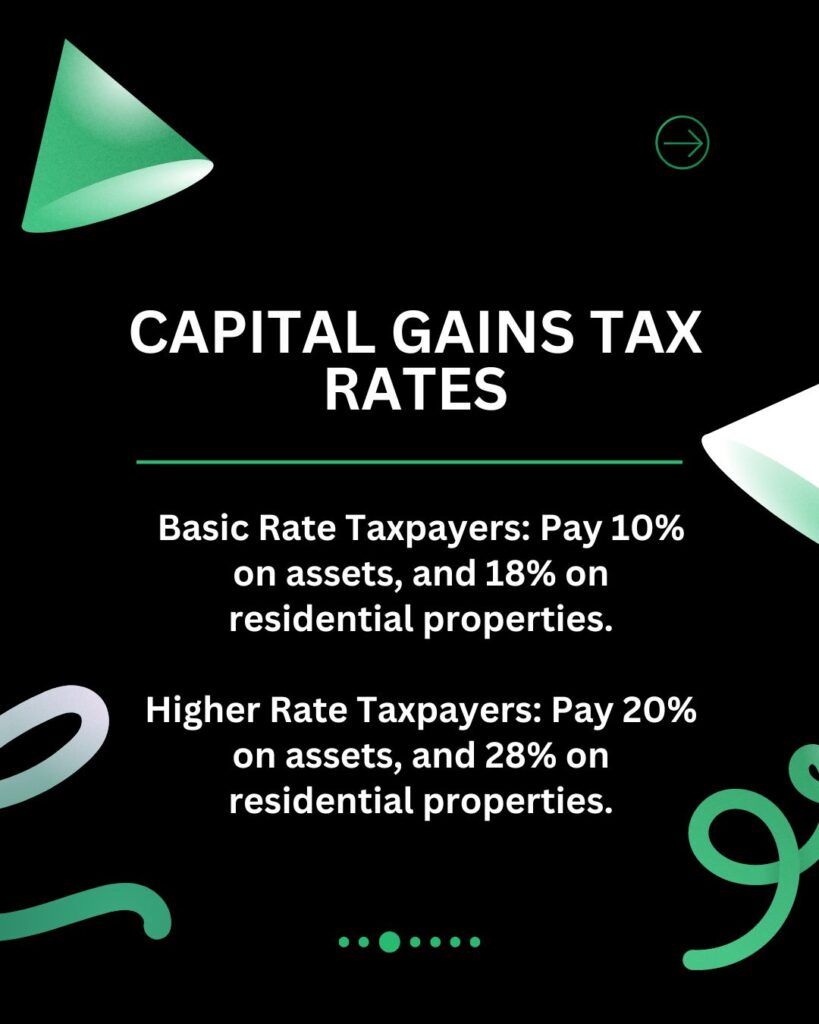

Capital Gains Tax Rates

There are two main rates of capital gains tax. These are:

- 10% Basic rate taxpayers

- 20% Higher rate taxpayers

With gains arising from disposals of residential properties, the 18 and 28% rates still apply. If you are entitled to Business Asset Disposal Relief, the tax rate is set at 10%.

If you’re entitled to Business Asset Disposal Relief (previously called Entrepreneurs Relief) the tax rate is 10%. This relief is generally only available when you sell a business. Unfortunately, the old 18% and 28% rates still apply to gains arising on disposals of residential property. They also continue to apply to “carried interest”, typically profits made by hedge fund managers and private equity managers. The 10% and 20% rates mainly benefit:

- Those disposing of commercial property (except where a business owner disposes of his trading premises and Business Asset Disposal Relief is available)

- Stock market investors (although many investors’ gains are tax free thanks to the £12,300 annual CGT exemption or by investing via an ISA or SIPP)

- Property investors who use a company to invest in property, when the company itself is sold or wound up

- Owners of trading companies who do not qualify for Business Asset Disposal Relief

Basic Rate Band

If you are a basic rate taxpayer, you can pay 10% or 18% capital gains tax on some or all your taxable capital gains. The 18% rate applies to residential property and the 10% rate applies to most other assets.

The basic-rate band is £37,700 this year (2021) so you can have up to £37,500 of capital gains taxed at these lower rates. It is important to note, the basic rate band will be £37,700 until the end of the 2025/26 tax year. You can only benefit from these lower CGT rates if your taxable income (for example your salary, rental income, or dividend income) does not use up your basic-rate band.

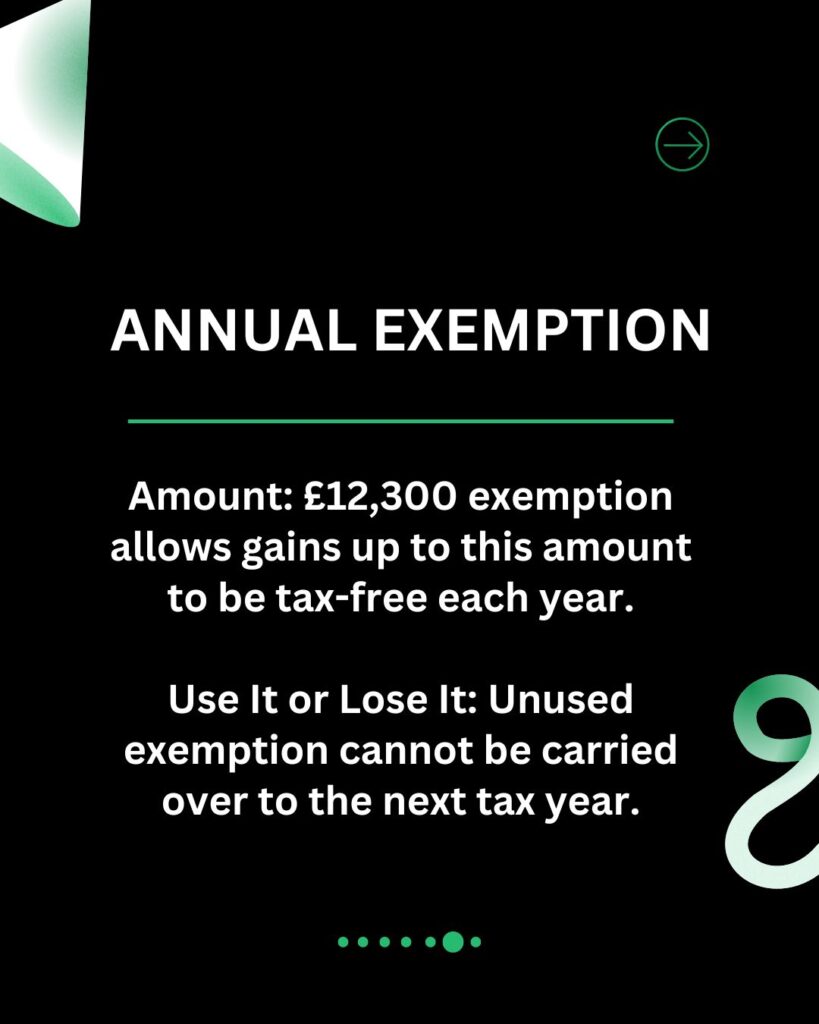

The Annual Capital Gains Tax Exemption

The annual exemption is £12,300. In other words, capital gains of up to £12,300 can be realised tax free during the current tax year. The exemption is fixed at £12,300 until the end of 2025/26 as part of the Government’s Big Freeze. Before the current freeze the CGT exemption had been increased by less than inflation for several years and, coupled with reductions in the basic rate band, means the Government has been increasing the CGT haul without increasing tax rates. Where possible, you should consider using this exemption before the end of the tax year on 5 April 2022. After that date, this year’s exemption is lost completely. It is essentially a case of ‘use it or lose it’.

Further Annual Exemption Benefits Couples enjoy one capital gains tax exemption each so they can have £24,600 of tax-free capital gains per year. Minor children also have their own annual exemption. The estate of a deceased person has its own annual exemption in the tax year of the death and the following two tax years. Trusts also have their own annual exemption equal to half of the annual exemption available to individuals (i.e., £6,150). However, this amount must be sub-divided amongst all of the trusts set up by the same settlor.

Contact us to find out more

Bed and Breakfasting

The old practice known as bed and breakfasting is no longer possible in its simplest form (selling assets, usually quoted shares, and buying them back the next day in order to utilise the annual exemption). However, there are still a number of ways in which the annual exemption can be used such as:

- Wait 31 days before buying the shares back. This strategy will not appeal to those who wish to remain fully invested.

- Bed and Spouse. Despite its name, this strategy can be used by all couples (married or not). One partner sells the shares and the other one makes an equivalent purchase. (For married couples and civil partners, the repurchase must be made on the open market – a direct sale from one spouse or partner to the other will not have the desired effect.)

- Bed and ISA – sell the shares to use your annual exemption and buy them back through an ISA.

Spreading Asset Sales

Property investors who want to sell more than one property should consider spreading their sales over more than one tax year, where possible, to use more than one year’s worth of CGT exemption. This will save a couple up to £6,888 per year in capital gains tax (£12,300 x 2 x 28%). Main Residence Relief Principal private residence (PPR) relief protects your main residence from capital gains tax. For disposals taking place from 6 April 2020 onwards it covers the period during which the property was your main residence and the last 9 months before selling (previously 18 months). Any property which has been your main residence and has been rented out at some point used to qualify for private lettings relief of up to £40,000 per person.

However, for disposals taking place from 6 April 2020 onwards private letting relief is restricted to periods where the owner is in ‘shared occupancy’ with a tenant. In other words, it is now restricted to periods when you are renting out part of your home while it is still your main residence.

Main Residence Relief

Principal private residence (PPR) relief protects your main residence from capital gains tax. For disposals taking place from 6 April 2020 onwards it covers the period during which the property was your main residence and the last 9 months before selling (previously 18 months). Any property which has been your main residence and has been rented out at some point used to qualify for private lettings relief of up to £40,000 per person. However, for disposals taking place from 6 April 2020 onwards private letting relief is restricted to periods where the owner is in ‘shared occupancy’ with a tenant. In other words, it is now restricted to periods when you are renting out part of your home while it is still your main residence.

Commercial Property Capital Gains

The main changes in recent times include:

- A reduction from 28% to 20% in the CGT rate applying to commercial property sales (18% to 10% where some of your basic-rate band is not used up by your income).

- CGT on non-resident capital gains. Until recently non-residents did not pay CGT when they sold commercial property located in the UK, for example offices, shops, warehouses and agricultural land. Commercial property gains that arise after 6 April 2019 are now subject to tax. Tax will only be payable on any increase in value from this date. They must file a non-resident capital gains tax return and pay the tax within 30 days of the sale.

Capital Losses

Capital losses are automatically set off against capital gains arising in the same tax year. Any surplus losses are carried forward to set off against future gains (but only to the extent that future gains exceed the annual exemption, so the annual exemption will not be wasted).

Generally speaking, capital losses may not be carried back to earlier tax years. The capital loss rules have a couple of important practical implications:

- Losses must be realised by 5 April 2022 in order to be set off against 2021/22 capital gains.

- If the losses you realise during the current tax year take your capital gains below the level of the annual exemption (£12,300), some of the annual exemption is wasted.

The timing of the disposal of assets standing at a loss should therefore be considered carefully.

Business Asset Disposal Relief

Business Asset Disposal relief was previously known as Entrepreneurs Relief. It allows each individual to have capital gains for a lifetime of £1million taxed at just 10%. In the March 2020 budget, the lifetime limit was drastically reduced from £10 million to £1 million which is what the current rate is set at.

As the lifetime limit is now a lot less generous than it used to be, it may now be necessary for you to spread assets among various family members to save CGT.

Who Qualifies for This Relief?

This relief is made to benefit owners of trading businesses which are essentially regular businesses.

A business will lose its trading status when it owns significant investments including any rental properties. If you are a property investor or simply own a few properties, the taxman does not treat you as a trading business owner, they will treat you only as a business owner.

Two types of property that can qualify for Business Asset Disposal Relief are:

- The trading premises of your own business, for example, a retail unit owned by a sole trader.

Business Asset Disposal Relief can also be claimed when your partnership or company uses a property that you own personally. However, it is important to note that there are restrictions that apply.

- Furnished holiday lets (in certain circumstances) Company owners are entitled to Business Asset Disposal Relief when they sell their shares.

The main qualifying criteria are the following:

- The company must be a ‘trading’ company

- The company must be your company. Generally, this means you must own at least 5% of said company

- You must be an employee of the company

Each of these rules must be satisfied for at least two years before the company is wound up or sold. Each of the rules must be satisfied for at least two years before the company has ceased trading. The disposal of the company should then take place within three years after trading has stopped. This time period used to be one year instead of two years. The new two-year rule applies for disposals taking place after 6th April 2019.

Investors Relief

This relief provides a 10% capital gains tax rate for investors in unlisted trading companies, providing they hold onto their shares for at least three years. Investors Relief only applies to gains on newly issued ordinary shares in unlisted companies. Buying shares from existing owners does not qualify. There is no minimum percentage shareholding. The relief is subject to a lifetime cap of £10 million of capital gains (unlike the £1 million cap now applying to Business Asset Disposal Relief). The investor generally cannot be an employee or officer of the company, and neither can any connected person (e.g., close family members).

However, the investor can become an unpaid director if he was not involved or connected with the company before investing. He can also become an employee 180 days after investing, providing there was no reasonable prospect of becoming an employee at the time the investment was made.

Contact us to find out more

Non-Residents

Quite a few years ago it was possible to leave the UK for a short period of time and avoid capital gains tax on any assets sold while non-resident.

The rules have now changed so that you have to remain a non-resident for at least five complete tax years in order to avoid any capital gains tax. Under the current anti-avoidance rules, to attempt to avoid capital gains tax your period of non-residence must last for more than five years.

This may mean you have to leave the UK for more than five years or you may have the option for less than five years, depending on whether ‘split-year treatment’ is available and whether you are treated as non-UK resident under the terms of a double tax agreement.

Over the last couple of years now, non-residents have had to pay CGT on some of their gains from UK residential property. Only the part of the gain arising after 5th April 2015 is subject to tax.

Recent Changes

Non-residents are also subject to capital gains tax on UK commercial property from 6th April 2019.

It is also important to note, where a non-resident sells shares in a company that derives at least 75% of its value from a UK property, the sale will now be subject to UK capital gains tax. The individual should own around 25% or more of the company.

Only gains arising after 5 April 2019 are subject to tax.

Reporting Capital Gains

You will need to report capital gains arising during the year on your tax return if:

- Your total sale proceeds for capital disposals made during the year exceed four times the annual exemption or,

- You have any capital gains tax liability.

If you sell a property and the gain is completely covered by the principal private residence exemption (e.g., the sale of your main home), it does not have to be reported on your tax return.

It is also very important to report capital disposals that give rise to an overall capital loss for the tax year, so that you can carry the loss forward to future years.

CGT Payments – Residential Property

Normally capital gains tax has to be paid by 31 January after the end of the tax year. From 6 April 2020, UK residents who sell residential property must make a pre-payment of capital gains tax (payment on account). This payment, along with the submission of a return, must be made within 30 days of the property’s sale.

Company Capital Gains

Indexation relief on capital gains made by companies has been frozen with effect from 31 December 2017.

This means that the relief available on disposals from 1 January 2018 onwards will be limited to the increase in the Retail Prices Index up to December 2017.

This is a major blow to property investors who hold investment properties inside a company and business owners who hold their premises inside a company.

Indexation relief has protected companies from paying corporation tax on any rise in a property’s value which is simply down to inflation.

Learn more: Related Articles

About the Author

Arun Mehra

With almost twenty years of commercial experience and knowledge in Dentistry, Arun’s expertise is valued by hundreds of businesses across the UK. His financial acumen and know-how, along with his hands-on commercial expertise have helped clients, large and small, new and established to achieve great things.

Arun is the founder of the Samera Group, starting the business with just one client sitting at his father’s dining table. Fifteen years on, Team Samera now service hundreds of Dental clients, run exciting events, help clients raise finance, and are very active in helping clients buy or sell Dental practices.

Further Information on Accounts & Tax

Our team of specialist accountants and tax experts can help manage, process and structure your business’s finances. From management accounts and payroll & pensions to tax planning and cash flow management, we can take care of the full back-office function of your business.

Book a free, no-obligation consultation with one of the team to find out how we can make your accounts & tax easier, quicker and cheaper.

Make sure you never miss any of our articles, webinars, videos or events by following us on Facebook, LinkedIn, YouTube and Instagram.